Retirement planning used to be simple:

work 40 years, save consistently, and rely on predictable returns.

But in 2026, the math has changed.

People are living longer, interest rates remain volatile, the job market is shifting fast, and investment patterns look nothing like they did 20 years ago. As a result, most traditional retirement formulas are outdated.

The good news?

There is a new, more realistic framework that gives you clarity — even if you feel behind or unsure.

It’s called The Range-Based Retirement Model, and it transforms how you calculate what you actually need for a secure future.

⭐ The Problem With “The Number” Thinking

Most people have been told to chase a single retirement number:

- $500,000

- $1,000,000

- $2,000,000

But this creates anxiety because life doesn’t follow a straight line.

Real retirement depends on:

- lifestyle

- inflation

- healthcare needs

- personal values

- where you live

- income flexibility

- part-time work

- investment timing

Your life is dynamic.

Your retirement plan should be too.

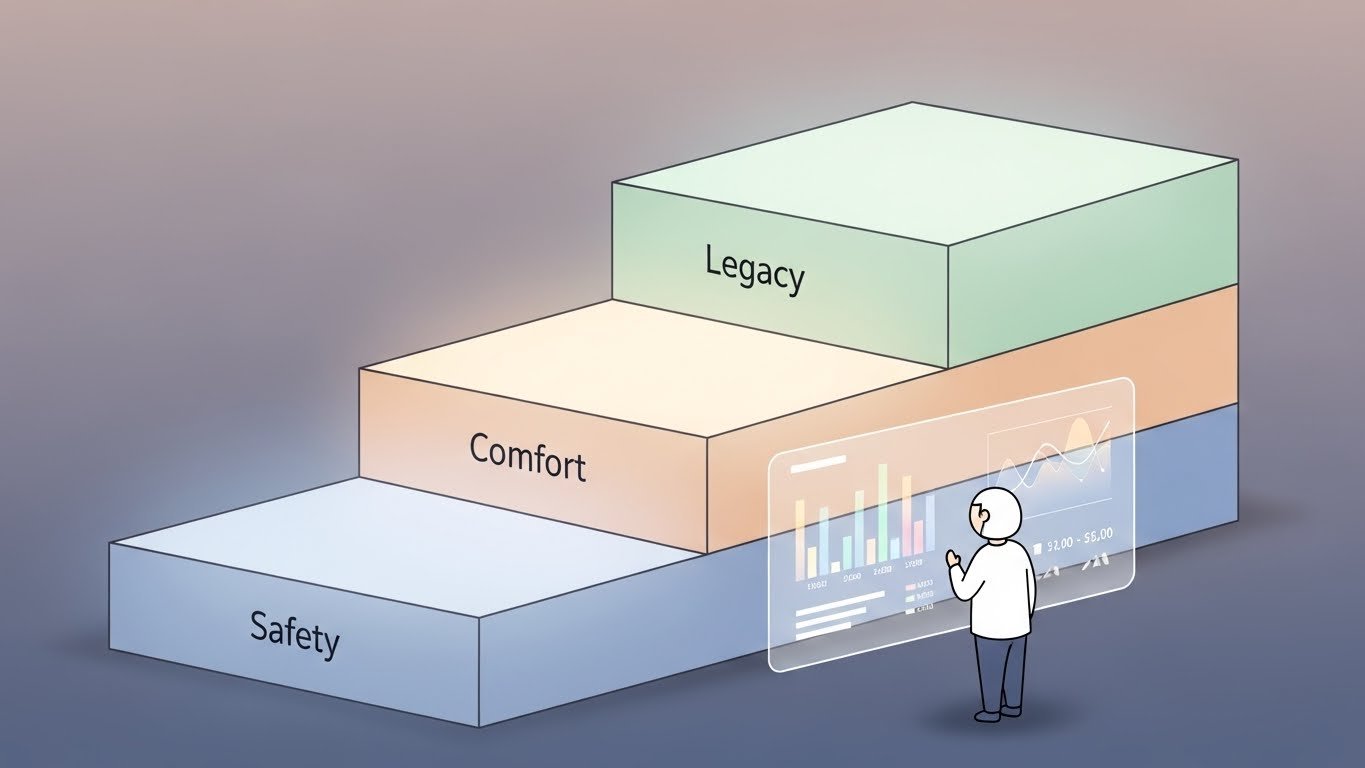

⭐ The Range-Based Retirement Model (2026 Edition)

Instead of chasing a fixed target, financially secure people use a simple three-tier structure:

1. The Safety Range (your absolute minimum)

This covers:

- rent or mortgage

- food

- transportation

- insurance

- essential healthcare

It’s the “zero stress” baseline.

2. The Comfort Range (your lifestyle zone)

This includes:

- travel

- hobbies

- dining out

- better healthcare options

- gifts and family support

This is where retirement begins to feel like freedom.

3. The Legacy Range (your wealth zone)

Here you fund:

- investments

- property

- charitable giving

- inheritance

- long-term family impact

Instead of one impossible number, you now have a realistic, flexible path.

⭐ The 2026 Retirement Equation

To calculate your range, use:

(Annual Expenses – Flexible Income) × 25 = Target Range

Flexible income can include:

- part-time or freelance work

- rental income

- dividends

- pensions

- Social Security

- seasonal consulting

This dramatically lowers your required savings.

Example:

If your expenses are $36,000/year and you expect $12,000/year in flexible income:

(36,000 – 12,000) × 25 = $600,000 Retirement Range

Not $1 million.

Not $2 million.

Just real math.

⭐ Why This Model Works in 2026

1. It adapts to income flexibility

Most retirees don’t stop working completely — they simply shift the way they work.

2. It reduces pressure

Knowing your Safety Range makes retirement feel achievable.

3. It reflects modern expenses

Travel, healthcare, and inflation fluctuate; ranges absorb the variability.

4. It aligns with current investment climate

Market volatility is normal — ranges give breathing room.

⭐ The Emotional Shift That Matters Most

People don’t retire when they hit a number.

They retire when they feel secure.

The Range-Based Model does exactly that:

- reduces anxiety

- increases control

- creates clear benchmarks

- prevents burnout

- motivates consistent saving

Retirement becomes a path — not a finish line.

FAQs

Do I still need to invest aggressively?

Not aggressively — consistently. Behavior beats timing.

What if I’m starting late?

Ranges make catching up realistic. You only aim for the Safety Range first.

Should I include my home equity?

Yes, but conservatively. Only count what you’d actually access.

Conclusion

Retirement in 2026 is no longer about hitting one magic number.

It’s about designing a personal system that fits your life, your habits, and your future.

When you understand your Safety, Comfort, and Legacy ranges, you stop guessing — and start planning with confidence.

Your retirement becomes predictable, flexible, and achievable.