Saving money has become one of the biggest challenges for American households. Rising housing costs, higher insurance premiums, increased interest rates, and inflation that still impacts daily life make traditional saving advice feel outdated. The old strategies — “cut back on coffee,” “spend less,” “hope there’s money left at the end of the month” — simply don’t work anymore.

In 2026, saving requires a new approach: one built on automation, psychology, better structure, and realistic financial planning. This longform guide shows exactly how to save effectively in a high-cost world, even if your budget feels tight.

Why Saving in 2026 Is Harder — But More Important Than Ever

Many Americans struggle to save because the financial landscape has shifted dramatically. Costs have risen, wages haven’t kept up evenly across sectors, and unpredictable expenses — from medical bills to car repairs — hit harder than before.

Saving is no longer just about preparing for long-term goals.

It’s about stability.

It’s about resilience.

It’s about preventing small emergencies from becoming financial disasters.

A well-designed saving plan protects you from uncertainty in an increasingly unpredictable world.

The Psychology of Saving: Why Most People Struggle

Saving is not a math problem — it’s a behavior problem. People don’t overspend because they lack intelligence; they overspend because:

• Digital shopping removes friction

• Subscriptions pile up invisibly

• Lifestyle comparisons increase pressure

• Emotion drives impulsive decisions

To save effectively, you must design an environment that supports good habits.

The Foundation: Pay Yourself First

The most powerful saving strategy is still the simplest:

Save before you spend.

Instead of waiting for leftover money, you automate a transfer into savings the moment your paycheck arrives.

Why it works:

• Removes emotional decision-making

• Establishes predictable progress

• Prevents lifestyle creep

• Makes saving a default, not a decision

Even small automated contributions build long-term momentum.

How Much Should You Save in 2026?

The right number depends on income and stability, but here is a realistic target framework:

Starter Goal: Save 5–10% of take-home income

Healthy Goal: Save 10–15%

Strong Goal: Save 20–25% (ideal for long-term planning)

If these numbers feel impossible, start with whatever you can. The key is consistency, not intensity.

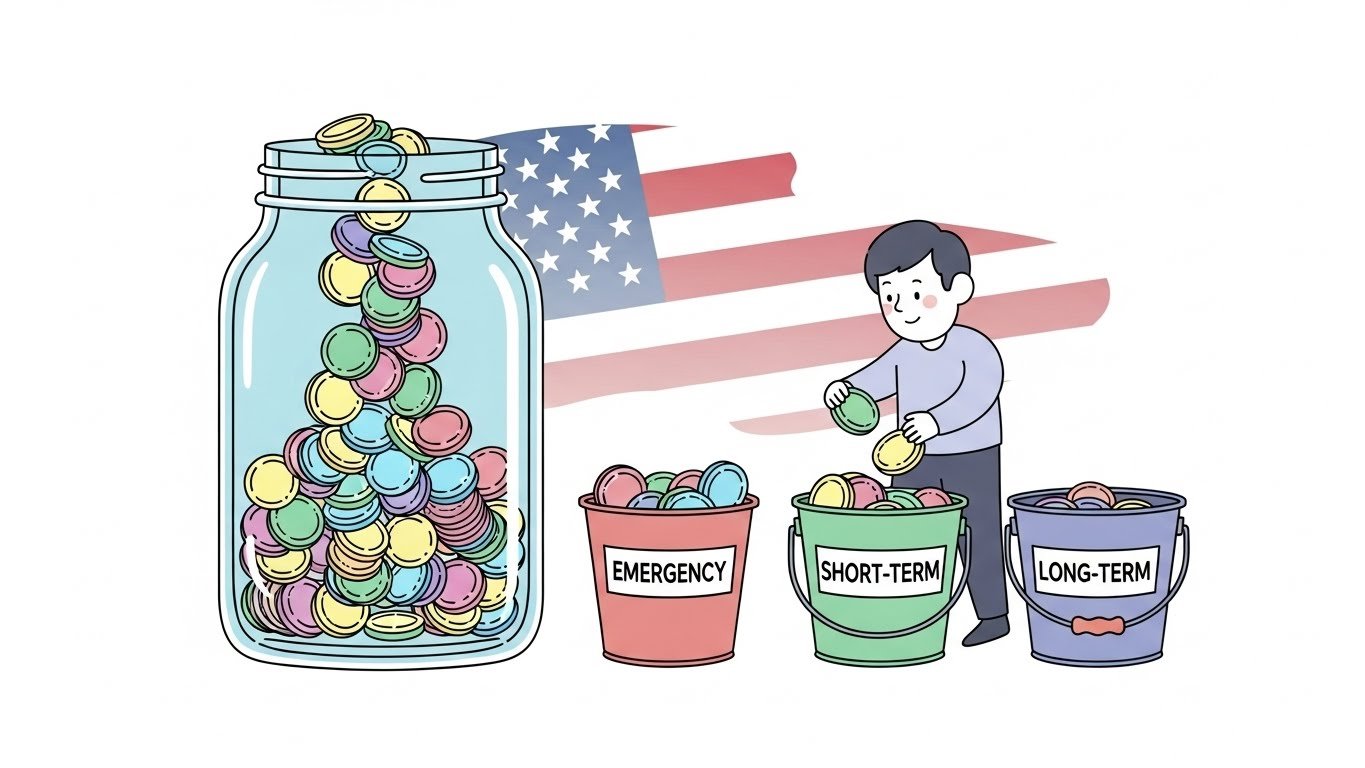

The 3 Essential Savings Accounts You Need

Having separate buckets prevents financial confusion and protects progress.

1. Emergency Fund

3–6 months of expenses stored in a high-yield savings account.

Purpose: stabilize your life during job loss, medical bills, major car repairs, or unexpected events.

2. Short-Term Savings (1–3 years)

Used for near-term goals such as:

• Travel

• Home repairs

• Car replacement

• Moving costs

• Holidays and gifts

This prevents you from dipping into emergency reserves.

3. Long-Term Savings (3+ years)

This includes retirement accounts, investments, or goal-based savings.

Where to Keep Your Savings for Best Results

Not all savings vehicles are equal. In 2026, the best options remain:

High-Yield Savings Accounts

The safest place for emergency funds.

Pros: FDIC insurance, liquidity, competitive APY.

Money Market Accounts

Good balance of yield and flexibility.

Certificates of Deposit (CDs)

Best for money you won’t need soon. Lock in higher interest when rates are attractive.

Treasury Bills

Safe, short-term government-backed returns.

Savings should grow — not sit idle. Choosing the right account protects money from inflation and increases financial stability.

The 2026 Saving Framework: The 4–Bucket System

This simplified approach is one of the most effective ways to structure your savings:

- Security Bucket: Emergency funds

- Growth Bucket: Investment-linked long-term savings

- Flex Bucket: Short-term planned spending

- Lifestyle Bucket: Travel, hobbies, experiences

This prevents budgeting fatigue and helps you allocate money with purpose.

Automation: Your Most Powerful Tool

Automation helps savers outperform those who rely on discipline.

Use it to:

• Transfer money immediately on payday

• Round up purchases into savings

• Trigger weekly micro-savings

• Set up sinking funds for recurring expenses

Automation reduces stress and increases results.

Cutting Expenses Without Feeling Restricted

True saving success happens when you create sustainable changes, not drastic cuts that burn out quickly.

Effective strategies include:

1. Audit Subscriptions

Eliminate duplicates or unused services.

2. Renegotiate Bills

Internet, insurance, and phone providers often match competitor rates.

3. Delay Upgrades

A 72-hour waiting rule prevents impulsive purchases.

4. Use Cash for Problem Categories

Cash adds friction and reduces overspending.

5. Increase Income Temporarily

Freelancing, tutoring, gig apps, or selling unused items can boost savings fast.

How to Save Even With Irregular Income

For freelancers and gig workers, the system must adapt.

Strategy: base your budget on the minimum monthly income, not the average.

All surplus income goes into:

• Emergency fund

• Tax account

• Retirement investing

• Short-term goals

This prevents financial whiplash during slow months.

How to Stay Motivated When Saving Feels Slow

Saving is long-term progress, not instant gratification.

To stay engaged:

• Track progress visually

• Celebrate milestones

• Name your savings goals (“Future Car Fund,” “Travel 2026”)

• Use habit stacking (save when you get paid, automatically)

Small wins matter more than perfect discipline.

TheDollarPulse Analysis

Saving in 2026 demands a new mindset: one built on automation, clarity, and adaptability. Cost pressures may be higher, but smart systems make saving achievable even for modest incomes.

The most important insight:

You don’t save with willpower — you save with structure.

When you automate, organize buckets, and remove emotional decision-making, saving becomes effortless. And over time, those small, consistent contributions become the foundation of true financial freedom.