Home insurance is becoming a flashpoint in household budgets in 2026. While national averages tell a calm story, homeowners in specific regions are seeing sharp premium increases, higher deductibles, and stricter coverage terms — sometimes all at once.

The reason isn’t just inflation. It’s risk.

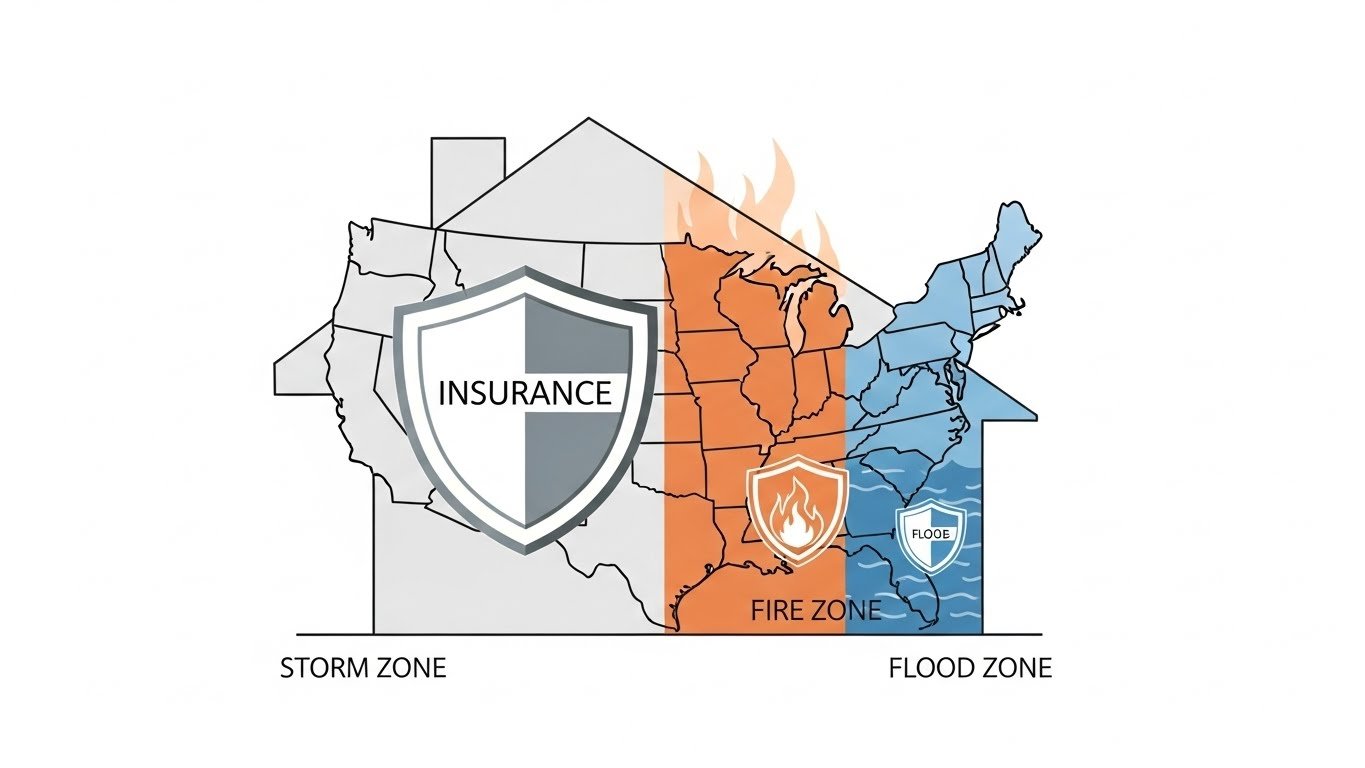

Why Home Insurance Is Rising Unevenly

Insurers are repricing risk with more precision than ever. Advanced modeling now weighs:

- Extreme weather frequency and severity

- Wildfire, flood, and storm exposure

- Repair and rebuilding costs

- Local claims history

- Reinsurance pricing

As a result, premiums are diverging dramatically by ZIP code.

Regions Seeing the Biggest Increases

The steepest hikes are appearing in:

- Coastal areas exposed to hurricanes

- Wildfire-prone regions in the West

- Flood-sensitive river basins

- Areas with rising construction costs

In some markets, insurers are also limiting new policies or exiting entirely.

Why Deductibles Are Rising Too

Higher deductibles help insurers control claims frequency. For homeowners, this shifts more risk out-of-pocket — reducing premium growth but increasing exposure when losses occur.

Many policyholders don’t notice deductible changes until a claim is filed.

How These Changes Affect Housing Decisions

Rising insurance costs influence:

- Mortgage affordability

- Escrow payments

- Home buying decisions

- Renovation and rebuilding plans

In extreme cases, insurance availability becomes a gating factor for homeownership.

What Homeowners Can Do to Reduce Impact

Practical steps include:

- Shopping rates annually (even if loyal)

- Adjusting deductibles strategically

- Reviewing coverage limits and exclusions

- Mitigating risk (roof upgrades, fire-resistant features)

- Bundling policies where it makes sense

Small adjustments can offset large increases.

Why This Matters for the Broader Economy

When insurance costs rise faster than incomes, housing markets cool unevenly. This affects mobility, pricing, and local tax bases — feeding back into regional economic differences.

What to Watch Next

Key indicators include:

- Insurer market exits

- Reinsurance pricing trends

- State-level policy responses

- Claims severity data

These will shape premiums going forward.

The Key Takeaway

In 2026, home insurance costs are no longer uniform. Understanding regional risk — and actively managing coverage — is becoming essential to protecting both homes and household finances.